General economic theory

In the first eighty years of the twentieth century there was a substantial growth of state activity. Economic regulation had grown rapidly after the economic crisis of 1930 when it was recognized by economists that the price mechanism in the Western society was not sufficient enough in order to achieve the major economic goals. At the same period, the mixed economy system was promoted under J. M. Keynes influential General Theory of Employment, Interest and Money in 1936 by which he showed that there is no reason to believe that the free working of price mechanism system will result in full employment.

The UK became a mixed economy with substantial public (government) and private enterprise sectors and there was a substantial government involvement in the private sectors, aiming at encouraging certain desirable trends as well as curtailing trends that were considered undesirable, although there has been a trend in 1979, during Thatcher Government for lesser state involvement (Jwell, 2000).

The UK government, in the context of the foremost duties and objectives of any government, is in command of the economy in such a way so as to attain certain economic goals such as, economic growth, price stability and full employment, balance of payments equilibrium and a rising standard of living for the general public.

According to Keynesian economists, these objectives can be achieved by regulating the level of aggregate demand. Demand can be managed by operating on any of the five variables which make up the aggregate demand, being the consumers, the firms investing in new equipment, the public sector, firms and governments abroad buying UK exports and less UK demand for imported foreign goods and services (Anderton, 1997).

The government can control and regulate these variables by injections and withdrawals of capital and at the same time by adjusting the weapons of Keynesian demand management which are taxation, government spending, interest rates and bank lending controls. This controlling and regulating action is denoted by the term “economic regulation.”

Regulation may be imposed by enacting laws and leaving their supervision to the normal processes of the law, by setting up special regulatory agencies or by encouraging self –regulation by recognising or delegating powers to voluntary bodies.

According to the National Economic Development Office (NEDO, 1975) successive UK governments have used the construction industry as an economic regulator.

The rational behind using construction industry as economic regulator

In order to examine the rational behind using construction industry as economic regulator, one should examine two main factors: The potential and effectiveness of the industry to influence the achievement of the major economic objectives of the government and vice versa, the potential and effectiveness of the government to influence the industry so as to gear it to the desired direction.

As it is argued by Ruddock (2007), «Valuing the construction industry, and assessing the importance of the industry to the economy as a whole is a difficult yet important task. Highlighting the importance of construction to the economy is a key point to ensuring it is a high priority for government agendas». Furthermore, according to the National Audit Office (NAO, 2001) the UK construction industry is a significant contributor to the national economy accounting for 8% of GDP and employing 1.9 million people.

The regulatory potential of the construction industry

The potential and effectiveness of the industry to influence the accomplishment of the dominant economic intent of the government is related to the following key characteristics and performance indicators: the activities, the size and structure of the industry as well as the performance of the industry measured in terms of its contribution to the UK GDP and employment and the quality of life.

The definition of the above characteristics depends on the definition of the industry, which is an aspect dealt with by several researchers, who consider it as a necessary prerequisite for studying the role of the industry in the economy. According to Pearce (2003), the construction industry has narrowed and broaden definitions: (i) The narrow definition confines attention to the on-site construction activity by contractors. In figure 1 hereunder, the narrow definition is shown within the bold lines. (ii) According to the broad definition, the true extent of the industry is broader than the above and includes the extraction of construction raw materials, the manufacture and sale of building materials, products and assemblies, the sale of construction products, and the various related professional services.

Activities and size of the industry

The industry is very large, including according to the narrow definition probably some 170,000 firms, whereas in the broad definition the number is closer to 350,000 (Pearce, 2003).

Figure 1: Broad and narrow industry definitions

Source: Pearce ( 2003)

According to the government’s department of trade and industry (DTI, 2004) for the year 2001 the construction industry covers 168,123 firms. This figure is in line with the UK National Audit Office (NAO, 2001) where 163,236 firms are noted for 1999.

The structure of the industry

The structure of the industry, as it is stated by the UK government’s department of trade and industry (DTI, 2004) is heavily skewed towards small firms. According to the National Audit Office (NAO, 2001) the number of employees of each firm is very small taking into account that 95% of the firms have 1-13 employees, producing according to DTI (2004), only a third of the sectors output and employ in total 43 % of the workforce) 4% have 14-79 employees and 1% have over 80 employees. In accordance with the DTI (2004) the largest contractors, account for less than 0,50% of the firms and produce 12% of the output and employ 10 per cent of the workforce.

Industry’s contribution to the employment

The construction industry is labour intensive and employing around 1.9 million people in 1999 out of which 500,000 were self employed (NAO, 2001). Figure 2 illustrates that in the broaden definition of the industry, in 2001 around 3 million people were employed (Pearce, 2003) and this corresponded to 10.7% of the total employment in the UK which was approximately 27.9 million (as of July 2003). The employees have an extensive array of different occupations, from bricklayers, electricians, plumbers and site managers to lawyers, surveyors, consulting engineers and architects. Unlike most industries, the vast majority of those employees work in very small firms regularly acting as subcontractors for the large developers. Government and industry initiatives are attempting to address the current skills shortage, and also health and safety issues.

Figure 2 : The labour force in the construction industry 2001

(all manpower) ( Pearce, 2003)

Industry’s contribution to the Gross Value Added and Gross DomesticProduct

According to NAO (2001), the Industry’s contribution to the UK Gross Value Added (GVA) was £65 billion in 1999 and the Contribution to the Gross Domestic Product was (GDP) 8%. On the other hand Pearce (2003) notes that in the narrow definition, contribution to the GDP was around 5% in 2001 (comparable with the health and education sectors) whereas, on the broaden definition, doubles to some 10% of the GDP.

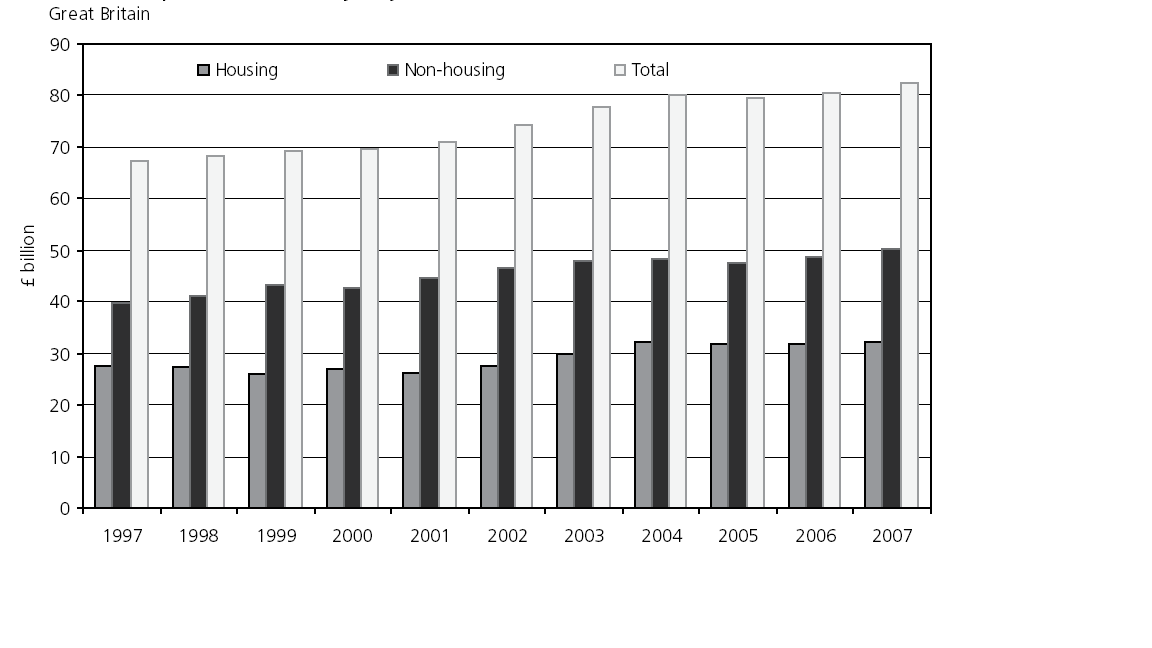

As it is illustrated in the Annex the industry’s output has been increased from about 65 billion pounds in 1997 to about 85 billion pounds in 2007, in constant prices of 2000

In light of the above it could be concluded that the industry’s contribution to UK GDP is between 8 -10%, depending on the way the industry is defined. According to DTI, the analytical breakdown of activity is illustrated in figure 3, hereunder.

Figure 3: Type of Construction Output, 2001

(R&Mstands for Repairand Maintenance)

The output of its main sectors accounts as follows:

- Non-Residential : 56% and at £22,6 billion

- Residential : 26% and at £10,6 billion

- Civil engineering : 18% and at £7,1 billion.

Pearce (2003) noted that the construction industry's contribution to man-made capital is substantial - a major part of the human created built - wealth in a country, comprises residences, workplaces, public buildings and infrastructure.

Figure 4: Value added per hour worked ($US)

The contribution of the industry to the GVA of the country could be increased through a government policy aiming at the increase of the industry’s labour productivity, as stated previously.. Figures 4 and 5 hereunder (DTI, 2004) illustrate that in 1999 there was a high productivity gap between the USA and the UK, France and Germany. On a labour productivity per hour worked basis, the UK is the least productive country. However on a person employed basis, UK productivity is higher than France and Germany after 1996, because UK average working hours are higher than in France and Germany (DTI, 2004).

Figure 5: Value added per person employed ($ ´000)

Ability of the government to influence the construction industry

Government departments and agencies can have a major influence on the construction industry as a sponsor, a regulator and a purchaser of building products ranging in size from £10,000 (typically repairworks for example, small flood defence projects) to £500 million (the British Library),NAO (2001). A critical factor in assessing the influence of the government over the construction industry is that some 37% of the industry's turnover is funded by the public sector which collectively makes it one of the largest clients, NAO (2001).

The consequences such policies may have upon the operations of those organisations and practitioners involved within the Construction Industry.

The conclusion from the above analysis is that the industry, due to its size and structure, as well as its output and its contribution to the employment of the country and the quality of life has the potential to produce a substantial «multiplier effect», as an economic regulator.

The «multiplier effect» mechanism can be used by the government for the increase of the employment, GDP and the National Income (expansionary fiscal policy), leading the economy from a recession into a recovery, through an initial injection (i.e. an investment) in the economy and in this case in the construction industry. Ultimately, the aforementioned creates more jobs, more output and more income in the industry that eventually creates more aggregate demand in the whole economy and so on - leading to the increase of the Aggregate Demand, employment, GDP and National Income.

The “multiplier effect” mechanism can be used in the opposite direction for curing an overheating economy, (contractionary fiscal policy) through a reduction of the government’s investment in the construction sector.

Government’s intervention may also take the form of an expansionary monetary policy through i.e. the reduction of interest rates and generally the increase of money supply or through a contractionary monetary policy in the opposite direction. In the former case, a rise in the interest rates (other things being equal) leads to higher mortgages and heavier financial burden and in due course higher construction products cost and prices, which eventually lead to a reduction of the demand for construction products as well as the employment and incomes in the construction industry and subsequently to a reduction in the Aggregate Demand, employment, GDP and National Income.

Government can also promote expansionary fiscal policy through the construction industry by providing state grants, and subsidies, i.e. to the low income people for buying houses or by providing tax relieves, i.e. to construction firms by the reduction of building licence fees.

In order to upsurge the industry’s contribution to the GDP and the multiplier effect, the government can take measures for the increase of the labour productivity of the industry, such as the provision of incentives for the training of employees and the technological upgrading of the construction firms. Failure of the Construction industry to improve its productivity (by embracing new technologies – new materials, IT, etc.) and consequently to improve the productivity factor of the whole economy, would be a considerable cost to the UK economy (Pearce, 2003).

In order to upgrade the quality of life of the population the government can promote (i.e. by regulations) good design of the built environment (private and public housing, infrastructure etc) which generally contributes to (i) The physical and mental health and wellbeing, good social relationships, reduced crime, and higher productivity, and (ii) the saving of energy, which is a vital environmental concern taking into account that all buildings – commercial, public, industrial and residential – account for half of energy use in the UK and half of carbon dioxide emissions (Pearce, 2003).

Adverse effects on the industry

Despite its usefulness, the above policy might have some adverse effects on the industry, the main of which are indicatively mentioned hereunder

The main weakness of using the industry as an economic regulator is the possibility to create a distortion of the market forces within the industry. So when, regularly, in a period of high economic growth the demand for industry’s products is expected to be increased, a reduction of the government’s investment in the industry struggling with an over-heating economy would lead - contrary to the expectations - to a fall in demand that could critically create chain negative reactions.

Recent recession in UK and globally, as well as in the early 1970s and 1990s have showed the hostile impact that the abovementioned distortion could have on the construction industry.

As stated by Lewis (1994) difficulties in the commercial property sector, which arose from the recession itself and the preceding boom in construction entailed marked losses for the UK banking industry. Thus for many UK banks it was the second time in 20 years that unfolded a scenario of rising property values and increasing lending, followed by falling values and a residue of bad debts.

The above negative outcomes, when combined with a reduction in the banks liquidity (promoted in the context of a tighter monetary policy for combating inflationary pressures), as it happened in the UK (or resulted from bad debts and not cautious bank lending) would lead to higher interest rates and increase in the debt burden of construction companies. Taking into consideration that companies in the construction industry are subject to a higher degree, in comparison with companies of other sectors, to the danger of cash flow problems, due to the fact that (i) on the one hand they use high debts to finance the construction of large projects and that high gearing ratios make them sensitive to interest rate swings, particularly in countries like the UK where most debt is at floating interest rates (Rowlatt, 1993; Artis & Lewis, 1993; Lewis, 1994; Miles, 1994) and (ii) the cash flow problem could render their ability to repay their loans and eventually lead many of them to insolvency.

According to Ball et al., 1998; Harvey & Jowsey, (2004), the collapse of the real estate development companies had negative repercussions for the equity market, the banking industry and the economy as a whole, due to the fact that they are by nature highly leveraged companies.

According to the Journal of Financial Management of Property there is a disproportionate share of insolvency affecting UK construction. In an industry that produces about 8% of the GDP, approximately 17% of company liquidations over the last 25 years have been of construction firms.

The problems get worse as a result of the government's competitive tender procedure, according to which the tender is granted to the bidder offering the lower price. In times of economic regression, when the construction firms are hardly trying to survive and keep their employees, they offer bidding prices so near to the margins that lead them into insolvency. In addition, the failed bidders are overburdened by the cost of unsuccessful bidding.

An additional problem is derived from the fact that the construction firms, for the purpose of gaining the necessary flexibility in order to adjust easily to the distortion of the marketforces, minimise their resources in personnel and materials and delegate the implementation of the projects to small sub-contracting firms. This situation might lead to low economies of scale and subsequently higher costs as well as a substandard quality of the products especially if there is also lack of communication and good management practices, between the delegating and the sub-contracting firm as well as high percentage of casual personnel with little experience, training and loyalty.

Indeed, the construction industry is a great economic regulator but should be used by the government in a thorough manner - taking the necessary precautionary policy measures - to ensure and maintain the smooth operation of the industry and avoid any negative repercussions for the economy as a whole.

Appendix

Output: New work and repair and maintenance

Constant (2000) prices, seasonally adjusted

Output: Housing and Non-Housing

Constant (2000) prices, seasonally adjusted